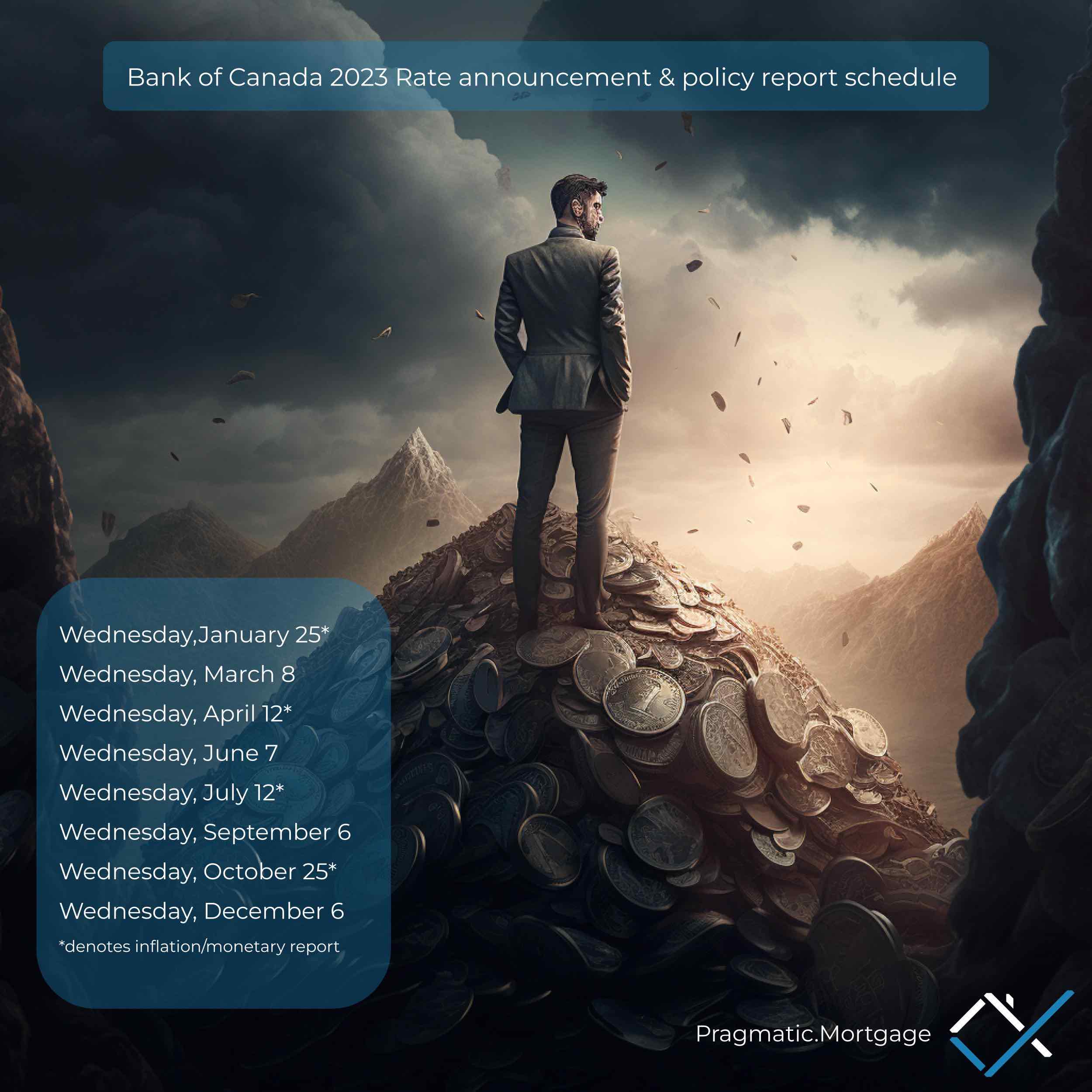

Co Guarantor Vs Cosignor | Which Option Should I Pursue?

Co Guarantor VS CoSignor

You apply for a Mortgage or Car loan and the bank says “sorry you need a CoSignor”. Without explaining WHY you need this it can be difficult to know which one is the best scenario to fit your needs.

See if a Co Guarantor Vs Cosignor is the right fit.

A Co Guarantor is when someone assists you with credit. However, a Co Guarantor does not OWN your asset nor do they use there own income to help you qualify. Thus a Co Guarantor is simply to assist in helping you if you have no credit or what is called “thin credit”. Most Guarantor strategies are a fit for newer corporations that have not obtained a credit history, so they use one of their directors on the board (CEO, CFO, COO etc) to guarantee the loan with their credit established.

A Co Applicant, also known as a CoSignor. Is much different. A CoSignor will use credit AND income to qualify. Plus they will also be entitled to ownership for the asset (be on title of property or vehicle).

A CoSignor is more common in a mortgage or vehicle purchase because likely you will need not just credit to qualify, but also extra income to get the debt service ratios in line!

Still Confused? A Co Guarantor Vs Cosignor each has their own pros and cons and are a right fit depending on the strategy.

Contact your Mortgage Broker today and explain the scenario you are trying to achieve. A good mortgage broker will make sure the short term and long term strategy is drawn out for you achieve 100% home ownership with NO Co Guarantor or Co Signor once possible.

kylewilson.ca bookpro.co hmcf.ca

#beincontrol #guarantor #cosignor #mortgage #mortgagebroker #homeownership #carloan #loans #mortgagemonday #asset #finance #money